Debt Relief Specialist wants to share a settlement letter from Amazon/Synchrony Bank. Bal. $3151.29 Offer $1103.00 Savings $2048.29

Debt Relief Specialist wants to share a settlement letter from Amazon/Synchrony Bank. Bal. $3151.29 Offer $1103.00 Savings $2048.29

Debt Relief Specialist wants to share a settlement letter from Bank of America. Bal. $1192.45 Offer $656.00 Savings $536.45

Debt Relief Specialist wants to share a settlement letter from Walmart/Synchrony Bank. Bal. $4620.21 Offer $1300.00 Savings $3320.21

Debt Relief Specialist wants to share a settlement letter from Citibank. Bal. $10,268.92 Offer $3594.12 Savings $6674.80

Debt Relief Specialist wants to share a settlement letter from Capital One. Bal. $12,528.75 Offer $4386.00 Savings $8142.75

Debt Relief Specialist wants to share a settlement letter from Bank of America. Bal. $15,117.00 Offer $9,100.00 Savings $6,017.00

If your credit report is less than squeaky clean, don’t despair. Regardless of how creditors may make you feel, it is not a judgment on you as a person, but simply a report on how you’ve handled your credit related financial obligations. You will need to take a few active steps to set the record straight for the future.

Once you are done with your Debt Settlement Program there are some steps that you need to take to improve your credit. It will take a little time but it will happen before you know it if you stick to the plan.

After all of your debt has been settled, you need to ensure that you pay your bills on time moving forward. Many creditors will consider lending to someone with some late payments, if recent records show that you’ve mended your ways. However, in some extreme circumstances like bankruptcy or tax liens, nothing has a greater negative impact on credit. The due date for a payment is when it has to be in the hands of the creditor, not postmarked. Anything more than 30 days late will hurt your credit standing and set you back again, often seriously. Keep in mind that one day past the due date is considered 30 days late.

When it comes to the number of credit cards you should have, fewer is generally better. Having a few clean, active charge accounts will boost your score. Remember to keep your balances lower than 35% of your credit limit, meaning if you have a $1000.00 limit on your credit card never have a balance higher than $350.00. Even if you pay the credit card off every month it will still be reporting to the credit bureaus as the high balance on the account.

Minimize your outstanding debt. Even if your debt is relatively small and your monthly payments are manageable, having outstanding debt is always a negative factor. Try to pay down your existing debt as quickly as possible within your budget limitations.

Time is sometimes your best ally. Although you will have late payments or other derogatory information on your credit report, the more time you can put between such negative information and a better record of on-time payments and low debt, the more favorable your credit profile will appear in the eyes of lenders. Although negative information can stay on your credit report between 7 and 10 years, every month that passes where you exhibit responsible credit behavior is a positive step.

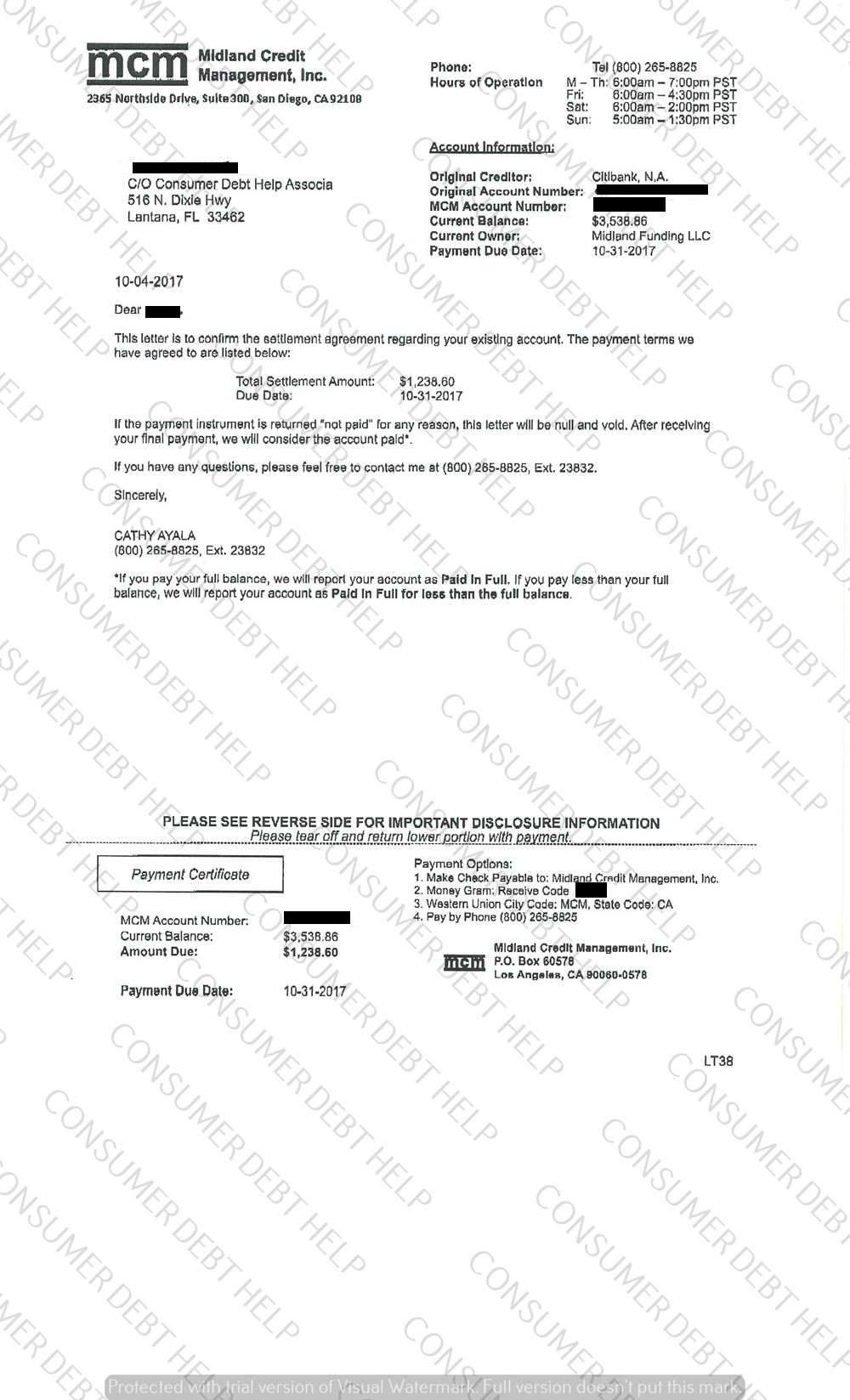

Debt Relief Specialist shares a settlement letter from Sears. Bal:$3538.86

Offer:$1238.60 Savings:$2300.26

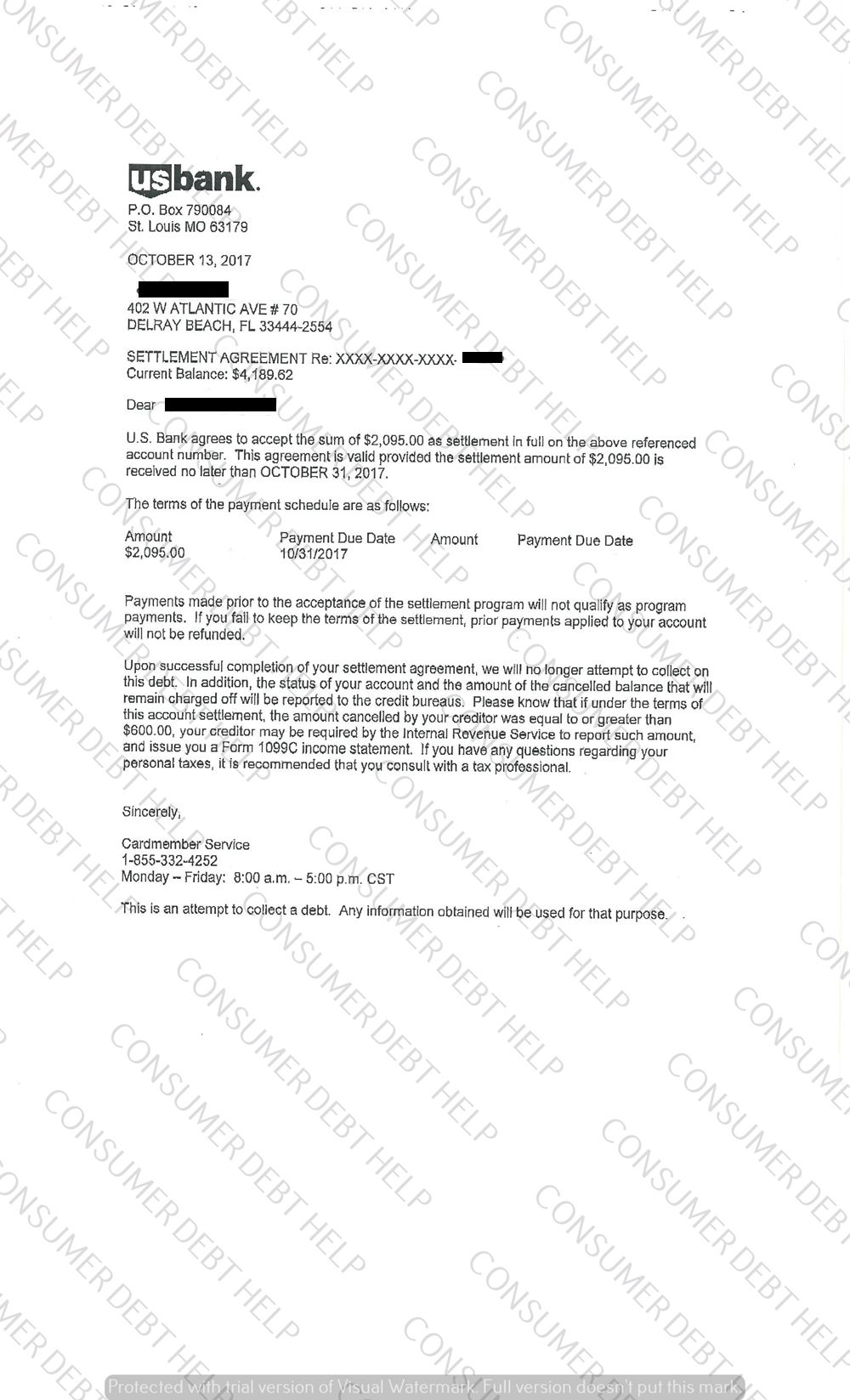

The Debt Specialist wants to share a settlement letter from US Bank. Balance $4189.62 Offer $2095.00 Savings $2094.62

copyright 2026 Consumer Debt Help Association - 516 N. Dixie Highway, Lantana, FL 33462. All Rights Reserved