Consumer Debt Help Association, Debt Relief Specialist wants to share a settlement letter from Citibank. Bal. $5685.40 Offer $1421.35 Savings $4264.05

Consumer Debt Help Association, Debt Relief Specialist wants to share a settlement letter from Citibank. Bal. $5685.40 Offer $1421.35 Savings $4264.05

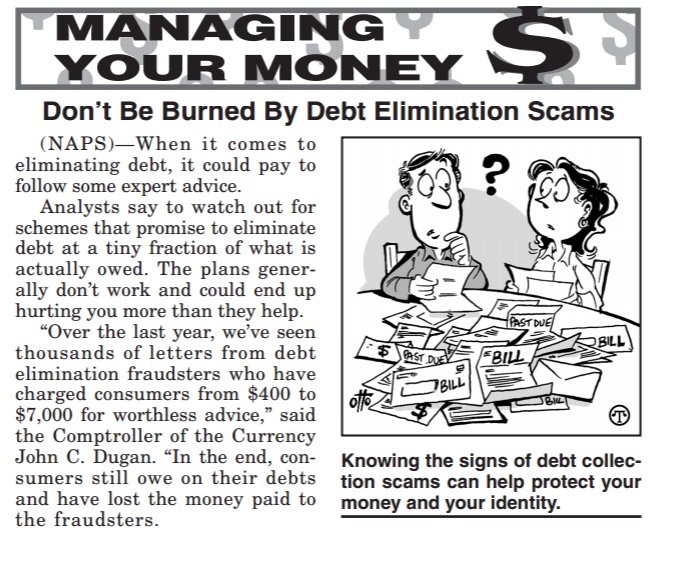

OCC Debt Elimination Notice

https://www.occ.gov/news-issuances/psa/dont-be-burned-by-debt-elimination-scams-feature.pdf

The Office of the Comptroller of the Currency (“OCC”) continues to see an increasing volume and variety of fictitious debt elimination schemes being perpetrated against financial institutions. These fictitious schemes are not to be confused with debt consolidation or debt workout programs presented by legitimate entities.

The object of legitimate programs is to assist the borrower to repay the debt in a responsible manner. The fictitious schemes claim to be able to “eliminate” or to “cancel” various types of debt from banks and non-banks without a material further amount of payment by the obligor. The fictitious schemes take various forms, including those that:

The fictitious, fraudulent schemes are being marketed to everybody, not just the wealthy or sophisticated, including borrowers who are current and those approaching foreclosure. The underlying fraudulent claim in all these fictitious schemes is:

These schemes are promoted: via the Internet; in seminars throughout the United States; and, directly by persons known to the victim by way of group affiliation, particularly religious and fraternal groups. These fraudulent schemes claim to “eliminate” or to “cancel” various types of debt, including mortgages, credit card balances, student loans, auto loans, and small business loans. All of them are simply designed to take an individual’s money, and are just the modern version of the old “up-front-fee” scheme. The schemes charge an up-front fee, or membership fee, that currently ranges from $400 to $7,500.

As a result of using a fraudulent scheme, individuals will lose money, could lose property, will damage their credit rating, and possibly incur additional debt. In addition, a creditor may take legal action against an individual to resolve a fraudulent attempt to eliminate debt. It is also possible for the victim to have identity theft occur by participating in a fraudulent scheme. The perpetrators of these schemes are known to steal identities and create substantial new debts in the victim’s name before they are even aware that it has occurred. It is extremely difficult and time-consuming to resolve the issues pertaining to identity theft.

These fraudulent debt elimination and cancellation schemes have no substance in law or finance. In statements and sometimes in the guise of education, the perpetrators of the schemes provide inaccurate or distorted information about applicable laws and real financial operations. The following are examples of inaccurate information the OCC has seen from these schemes:

There are unlimited variations to these schemes. The basic idea of these schemes, however, is to fool individuals into paying money to have a debt eliminated or cancelled, or to obtain false documents and the instructions on how to submit the false documents to creditors. The following are some variations of the false documents used:

Any information that you have concerning fraudulent debt elimination or debt cancellation schemes should be brought to the attention of appropriate local or Federal law enforcement personnel.

If the fraudulent scheme is presented via the Internet or e-mail, contact the Internet Crime Complaint Center (IC3). Please go to the IC3 Web site at http://www.ic3.gov and follow the instructions for filing a complaint (IC3 was f/n/a the Internet Fraud Complaint Center- IFCC). Contacts from other sources, such as individual contacts or seminars, should be reported to the local office of the FBI and your local financial fraud law enforcement organization.

If any portion of the offering or subsequent portions of the transaction are processed through the United States Postal System (USPS), the Criminal Investigation Division of the USPS should be contacted. Contact information can be obtained from your local U.S. Post Office.

A debt settlement company will be 1 year or longer term business partner. Monthly updates are routine for a solid partner. Use these other areas to help you assess your possibilities. Before you begin make this your “First Action Item”

Contact the BBB of its corporate headquarters city to see if they are a member. Is the debt settlement company a member of the Better Business Bureau? How highly are they rated. A+ is the highest and rare among this industry? Do they have complaints in the last year , 2 years, life time ? How long have they been in business. These simple steps assist your verifying the reputation of a qualified debt settlement company. After you find an A+ rated company explore the areas below.

While this list is offerred for your education and comments, we think the best way of measuring a client is how you are treated from enrollement to completion. So if that first call sends up any warning signals trust your inner self.

copyright 2026 Consumer Debt Help Association - 516 N. Dixie Highway, Lantana, FL 33462. All Rights Reserved