Debt Relief Specialist wants to share a settlement letter from Care Credit/Synchrony Bank. Bal. $2336.51 Offer $700.95 Savings $1635.56

Debt Relief Specialist wants to share a settlement letter from Care Credit/Synchrony Bank. Bal. $2336.51 Offer $700.95 Savings $1635.56

Debt Relief Specialist wants to share a settlement letter from American Express. Bal. $9560.34 Offer $2964.00 Savings $6596.34

Debt Relief Specialist wants to share a settlement letter from Credit One. Bal. $2959.65 Offer $1040.00 Savings $1919.65

Debt Relief Specialist wants to share a settlement letter from Citibank. Bal. $10,268.92 Offer $3594.12 Savings $6674.80

Your credit score can raise your rates on credit cards, auto loans, mortgages, and even your auto insurance. In some cases, it can keep you from getting a job or renting an apartment. So if you have a low credit score, rebuilding it to acceptable levels is very important. Since the formulas for credit scores are private, there’s much speculation as to how to restore your credit score.

To help us separate the fact from fiction, we put together this Q and A form. Once you complete your program your score will definitely go up but there are things that you could be doing to help the process along.

Q: What’s the biggest misconception about repairing your credit score?

A: The biggest misconceptions about repairing your credit scores is that it’s either impossible or will take many years, if not decades, to do. While it’s true it can take a substantial amount of time, it’s possible to go from bad to excellent credit. One of the best places to start is to check and track your credit scores and reports. Although you get one free copy of your credit reports (Experian, Equifax and TransUnion) from AnnualCreditReport.com each year, checking it once per year won’t help you track the progress. That’s where a credit report monitoring service steps in. With these services, you’ll receive alerts if there is a change, such as a new line of credit or a change of address, to your credit reports. Additionally, you’ll be able to track the progress of your credit scores. Contrary to what many believe, checking your credit reports and scores with these services won’t hurt your scores.

Q: Besides paying bills on time, what can be done to shorten the time it takes to boost your credit score?

A: In addition to paying your bills on time, paying your bills in full is a great way to shorten the time it takes to boost your credit score. Lowering your credit utilization ratio, which helps determine 30% of your FICO scores, will help drive up your scores. Your credit utilization ratio is a comparison of your debt to your available credit. The ratio is based on revolving debt (basically credit cards), rather than total debt. To calculate it, take your total amount of credi8t card debt and divide it by your total amount of available credit. This will give you a percentage or your credit utilization. For example, if you have $3,000 in credit card debt and $10,000 in available credit, your credit utilization is 30%. The lower your credit utilization, the better impact it has on your credit scores. Try to never be more than 30% credit utilization. Finally, addressing errors on your credit report can help improve your score once they’re resolved with the credit bureaus.

Q: What if a score is low because of errors or bills that the consumer doesn’t believe are owed?

A: It’s important to immediately report any errors that you spot on your credit reports. This will not only help boost your credit scores, but also potentially protect your identity. While these errors or incorrect bills may seem like harmless mistakes, they could also be a sign that you have fallen victim to identity theft, which is when someone uses your personal information to gain access to money, credit cards, or any other financial gain. That’s why it’s essential for you to report any errors as soon as you spot them. To do this, you’ll have to contact each of the three bureaus (Experian, Equifax and TransUnion) and follow its error-removing procedure. It’s also important for you to follow up with each of the bureaus after you have completed the request to make sure it has successfully been removed. Additionally, if you’re unable to get a mistake removed from your credit reports, you can get help from the Consumer Financial Protection Bureau for free or enlist a credit repair service, which will charge you a fee.

Q: Is getting a prepaid or debit card a good way to begin rebuilding credit?

A: No, prepaid or debit cards have no impact on your credit because the activity is not reported to the credit bureaus, which makes them no help if you’re trying to rebuild your credit. Instead, a secured credit card is a better option for you. These cards look and act as a regular credit card, but function a little differently because they are designed to help people with less-than-perfect credit raise their scores. When you open a secured credit card, you’re required to put down a security deposit, which will be used if you don’t pay your bill. If you maintain a good history with secured cards they will raise your credit limit without requiring an additional deposit. To start your credit limit will be based on the amount you put down as a security deposit. Additionally, unlike traditional credit cards, most secured credit cards report to all three credit bureaus, which makes it easier for you to raise all three of your credit scores. If you decide to apply for a secured credit card, make sure it’s one that reports to all three bureaus. Just keep in mind also that the deposit is non refundable, meaning no matter how long you have the card they will keep the deposit. If you ever close your account you will then get your deposit back but it is not recommended to close credit accounts.

Q: Does being on time with car payments or rent help your score?

A: Paying any sort of loan, including a car payment, on time will help improve your credit scores because loan payments are reported to the credit bureaus and tracked on your credit reports. On the other hand, rent doesn’t have an impact on your credit scores because it’s not sent to the credit bureaus unless you default on making your payments. This means not paying your rent will hurt your credit score, but paying your rent on time doesn’t raise it in most cases.

If your credit score has taken a hit, rebuilding it is an important part of financial success. Knowing more about what to do to rebuild your score should make the process quicker and easier.

We hope this article helped you, there are many tools out there to rebuild your credit but the main thing to keep in mind if nothing else is to always pay on time, and try and keep the amount that you borrow to the smallest amount possible to keep your credit utilization low. It is good to have different types of credit like having a car loan, credit cards, a mortgage, by only having credit cards will not allow your credit score to improve as greatly as it can with multiple types of credit. Sounds weird but you have to use credit, borrow money, to get better credit.

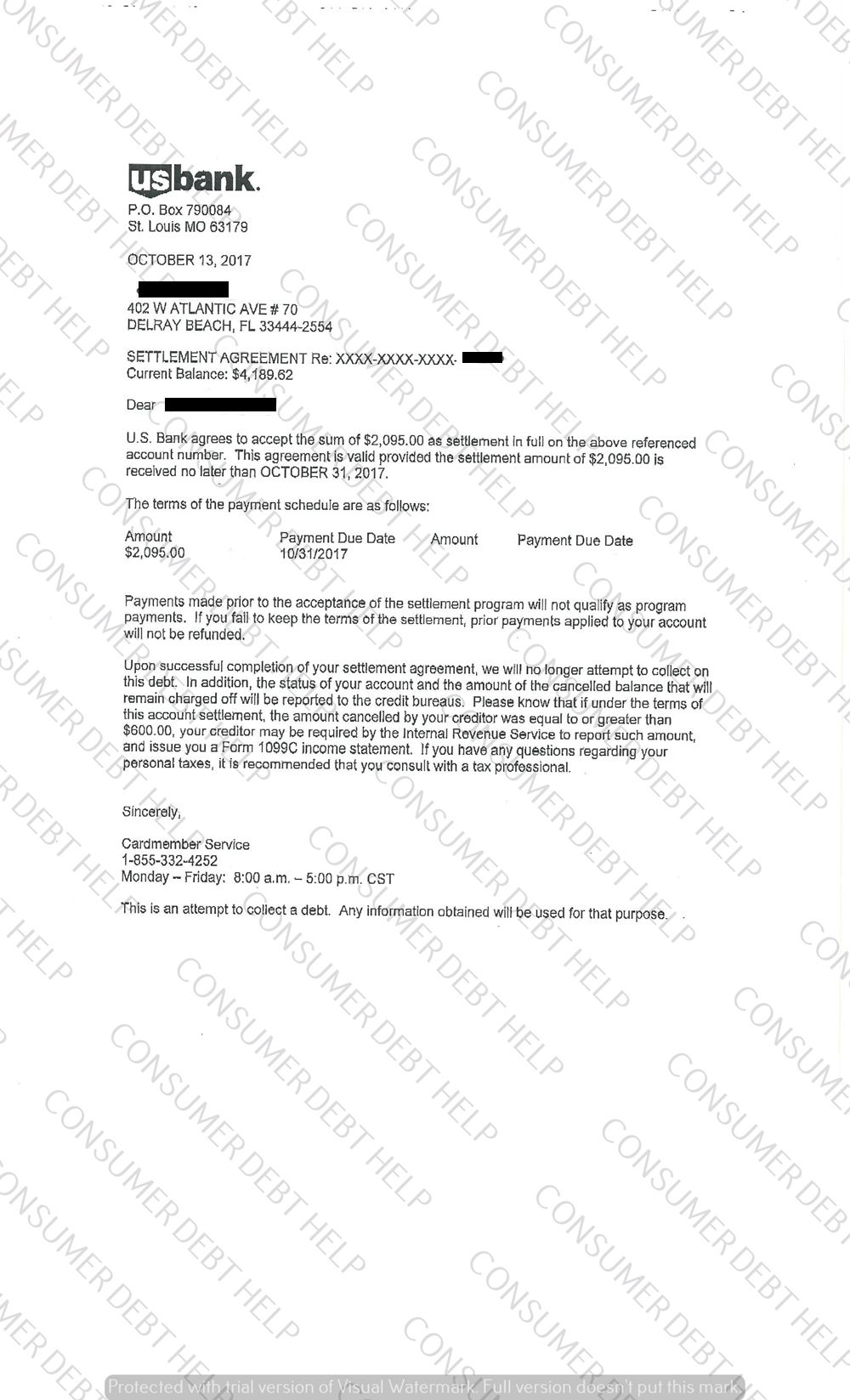

The Debt Specialist wants to share a settlement letter from US Bank. Balance $4189.62 Offer $2095.00 Savings $2094.62

Debt Relief Specialist wants to share a client review from today. –

–

copyright 2025 Consumer Debt Help Association - 516 N. Dixie Highway, Lantana, FL 33462. All Rights Reserved