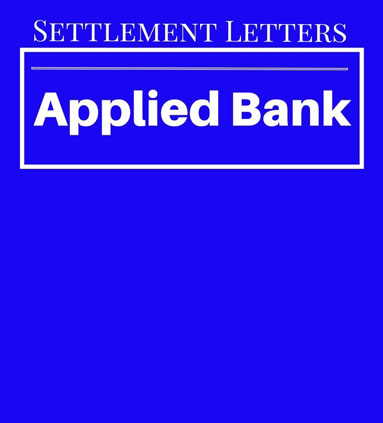

Debt Relief Specialist wants to share a settlement letter from Applied Bank. Bal. $2373.34 Offer $878.13 Savings $1495.21

Debt Relief Specialist wants to share a settlement letter from Applied Bank. Bal. $2373.34 Offer $878.13 Savings $1495.21

Debt Relief Specialist wants to share a settlement letter from Pen Fed Credit Union. Bal. $40,848.82 Offer $19,641.80 Savings $21,207.02

The holidays can put a financial burden even on the savviest of shoppers and savers. But like most things, taking time to plan can help you avoid the stress that comes with overspending. Before you hit the mall or shop for Black Friday deals, keep reading to learn how to make a holiday spending plan that works for you.

1. Set a budget

First, make sure you account for all of your typical expenses so that you don’t come up short on bills or things like rent. Next, think about what else you may be spending on in the coming months. Are you hosting a party at your home, or traveling to visit family or friends? If so, estimate what those things will cost you. Once you’ve subtracted any expenses from your usual budget, you can think about how much you have to spend on gifts. It’s best to start planning this as early as possible. That way you can look at how much you’ll earn between now and the holidays and calculate how much you can save to cover your holiday spending. Being realistic about your budget will help make sure you don’t overspend.

2. Make a list (and check it twice)

With all of the excitement of the holidays, it can be easy to get carried away. Make a list of the gifts you need and cross them off as you go. Check your list several times before you go shopping so that you don’t leave anything off. This is when a personal rule may come in handy. You might set a personal rule for yourself, such as: If something isn’t on your list, don’t buy it. This can get difficult when you see sales and deals pop up—but spending on something you don’t really need can make it difficult to pay for the things you do.

3. Get creative

There may be ways to give a meaningful gift at a fraction of the cost as buying something from a store. This may not work for everyone on your list, but here are some low-cost suggestions that CFPB employees have used:

•Homemade mixes in a mason jar, such as hot chocolate, bean soup, or cookie mixes

•You favorite recipes with photos in a custom picture book

4. Decide how you’re going to pay

Are you going to use cash or credit cards to pay for gifts? A helpful rule to set for yourself is to only bring the amount of money you plan to spend. That way you can help yourself stay within your budget because once you spend the money you brought, you’re done. On the other hand, using a debit card can give you more consumer rights if the item is broken when you open the box and doesn’t require you to travel with large amounts of cash. If you do decide buy your holiday gifts with a debit card, make sure you dont overspend and have set aside enough in your budget to do so.

5. Track your holiday spending

Just like you wrote down your lists to keep track of what you need to buy, you could also keep track of what you’ve spent. Periodically check to see if you are on track and sticking to your budget. Did you spend more or less than you thought you would on certain items? If you don’t keep track of what you spent, you could end up with an unpleasant surprise if you exceed your budget.

Stress is something most of us are all too familiar with. People turn to a variety of activities to help them cope with stress. Over eating, indulging in unhealthy snacks, and excessive or compulsive shopping are just a few stress-relieving behaviors that can adversely affect your health or seriously damage your budget. The suggestions listed below are offered as healthy, budget-friendly ways to relieve stress.

1.Take a hike. Sometimes just a walk down the hallway at work or a walk around the block can provide relief from a stressful moment. Incorporating a regular, mind-clearing walk into your daily routine is a great way to relieve stress.

2.Meditation is an ideal way to relieve stress. All that you need is a quiet place and a few moments and you can experience the peacefulness that meditation offers. You can find tips for learning how to meditate at websites such as StopAndBreathe.com. You may find it helpful to create a meditation space in your home or yard.

3.Listening to music is a great way to relieve stress. Some people find soothing music the best form of stress relief. For others, the best stress relieving music is something lively that they can sing along with or dance to. Find what works for you and let the music take away your stress.

4.Observation and distraction are ways to reduce stress that cost you little or nothing. When you’re feeling stressed about something, find an object or activity to focus on and give it your undivided attention. Everything from watching a sporting event to watching activity at a bird feeder fits into this category. If you’re stressed over a problem, you will often find that if you allow something to distract you from that problem, a solution will come to mind. A hobby, a phone call to a friend, a housecleaning frenzy or numerous other activities can be stress-relieving distractions.

5.Those that enjoy a frugal lifestyle are always interested in things that are both beneficial and inexpensive. Laughter is a wonderful way to relieve stress. George Gordon Byron advised, “Always laugh when you can; it is cheap medicine.” That frugal advice is still relevant today.

6.You can find numerous statistics that support the fact that pets help relieve stress. One source of information relating the positive benefits of pet ownership is HelpGuide.org. Here you will find information regarding the many therapeutic benefits a pet provides. A dog makes a great companion on a mind-clearing, stress reducing walk.

7.A very inexpensive form of stress relief is journal writing. There are various ways to approach the process of journaling to relieve stress. An excellent source of inspiration and guidance can be found at EverydayHealth.com.

8.Exercise has been described as “meditation in motion.” According to the information provided at MayoClinic.org, exercise has some direct stress-busting benefits. Following the tips offered by the Mayo Clinic staff can get you headed in the right direction when it comes to setting up a stress-busting exercise routine that is best for you.

The previously mentioned stress-reducing ideas involve little or no financial investment. They do require action and commitment on your part. Ultimately, finding and implementing ways to relieve stress is a personal process. You stand to gain in various areas of your life when you engage in stress-relieving activities that have health benefits and are emotionally uplifting.

Did your bank recently send you a new credit or debit card with a shiny, metallic chip on the front? You may have noticed that some cards have this chip in addition to the standard magnetic stripe on the back of the card. Lately, we’ve received questions from people wanting to know what these chips are and how they work. Because security is often people’s number one concern, we’ve also heard from consumers who want to know what they can do to protect their bank accounts, credit cards, and personal financial information.

As a new federal agency, we’re committed to providing you with trustworthy information about consumer financial products—including bank accounts and credit cards. Here are a few things you should know about chip technology.

What’s chip technology?

Chip technology is designed to help cut down on credit and debit card fraud. The technology has been in use in other countries for some time.

For credit and debit cards to work, they have to provide information—your so-called “payment credentials”—to the merchant that takes your card. The merchant uses that information to authorize the transaction. This is what that magnetic stripe, also known as a “mag stripe,” on the back of your card currently does. That’s what the new chips will do, too.

Why does this matter to me?

For consumers, the important difference between chips and mag stripes is that it’s more difficult for a fraudster to make a fake chip card than to make a fake mag stripe card.

The shift to chip cards won’t affect your legal rights that protect you from credit card and debit card fraud. But to be fully protected, you must still review your credit card and debit card statements regularly—and report fraudulent charges immediately. We have some practical suggestions for how to continue to protect your accounts below.

How do I use my chip card?

Instead of swiping your card through the payment terminal, with a chip card, you insert the end with the chip into the slot at the front of that terminal. You do this with the front of the card (and the chip) facing up. Terminals take slightly longer to read a chip card than a mag stripe, so wait for the terminal’s instructions before you remove your card.

Where can I use my chip card?

Not every place you shop will be able to read chip cards yet. If the store accepts credit and debit cards but doesn’t have terminals that can read chip cards, you can still shop there. You’ll just need to use the magnetic stripe on the back of your card. Over time, you’ll see more and more terminals that read chip cards.

What about online and mobile payments?

You can use your chip card to make mobile or online payments the same way you you’ve been using your old card.

Why is this happening now?

There’s no law requiring your credit card company to give you a chip card. That’s true for debit cards as well. Likewise, there is no law saying that stores have to install terminals that can read chip cards—or turn on chip card technology even if they do have these terminals.

Even so, you’re going to see a lot more chip cards and chip card readers in the months to come. Beginning in October, card companies and stores are changing how they divide up responsibility for card fraud. Those changes are creating incentives for merchants to install chip card terminals and for banks and credit unions to issue chip cards. So, a lot of card companies and merchants are rolling out this technology as soon as they can.

What if I don’t have a chip card yet?

You can still keep using your card, and you’ll be able to swipe your mag stripe through card readers. Keep in mind that your bank or credit union will most likely send you a chip card in the future.

How you can protect your accounts

The shift to chip cards is an important step in combating fraud, but experts agree that chip cards are not going to make card fraud go away. Fraudsters will still try to make money by stealing card data, and you’ll still need to protect yourself by taking some basic precautions:

• Check your accounts for unauthorized charges or debits regularly. Sometimes fraudsters will process a small debit or charge against your account and return to add more charges if the first transaction goes through. If you have online or mobile access to your accounts, check your transactions regularly. If you receive paper statements, be sure to open them and review them closely.

• Report a suspicious charge or debit immediately. Contact your bank or card provider immediately if you suspect an unauthorized debit or charge. If a thief charges items to your account, you should cancel the card and have it replaced before more transactions come through. Even if you’re not sure that PIN information was taken, consider changing your PIN just to be on the safe side.

Watch accounts closely when account data is hacked and report suspicious charges

If a thief takes money from your bank account by debit, or charges items to your credit card, you should cancel the card and have it replaced before more transactions come through. You should also consider changing your PIN just to be on the safe side.

Your best step to protect yourself from unauthorized charges or debits to your accounts is to report that your card or your information has been lost or stolen promptly after you learn of it.

For credit cards

If your account number, not your physical credit card, has been stolen, you are not responsible for unauthorized charges under federal law.

For debit cards

If an unauthorized transaction appears on your statement (but your card or PIN has not been lost or stolen), under federal law you will not be liable for the debit if you report it within 60 days after your account statement is sent to you. But if the charge goes unreported for more than 60 days, your money, and future charges by the same person, could be lost. There are timelines for the bank to investigate and recredit the missing funds to the account after you make a timely report about the problem.

The time for you to report is much shorter if your card or PIN has been lost or stolen (2 business days, in order to limit your liability to no more than $50 of unauthorized charges), so make the report as soon as you learn that your card is missing or your PIN has been stolen.

For payroll, government benefit, and prepaid cards

For these types of cards, your rights vary depending on the card. If you suspect information from a payroll, government benefit, or prepaid card was stolen, check with the provider to find out its policy and deadlines for disputing charges. Your rights vary depending on the type of card.

You can also learn more about your card protections at

consumerfinance.gov/askcfpb.

How to report a suspicious charge or debit

If you spot a fraudulent transaction, call the card provider’s toll-free customer service number immediately. Ask how you can follow up with a written communication. Your monthly statement or error resolution notice also likely includes instructions on how and where to report fraudulent charges or billing disputes.

When you communicate in writing, be sure to keep a copy for your records. Write down the dates you make follow-up calls and keep this information together in a file.

Tip: If you get a replacement card, remember to update any automatic payments linked to the card.

Information About the Equifax Data breach

On September 8, 2017, Equifax, one of the major credit reporting agencies, announced a breach that occurred from mid-May through July 2017. During this period, hackers accessed people’s names, social security numbers, birth dates, addresses, driver’s license numbers, and credit card numbers.

Equifax set up a website for consumers to check if their information was exposed: www.equifaxsecurity2017.com . This website has not been verified by regulators, but may provide pertinent information to consumers trying to determine whether they have been effected by the breach. To use the website, customers should click the “Potential Impact” tab, enter their last name and the last six digits of their social security number. Customers are urged to take standard precautions, including using a secure computer and an encrypted network connection, when accessing the website.

Management can proactively mitigate the fallout from this and other breaches by ensuring the following:

The Federal Trade Commission released some steps to help consumers after the data breach, as follows:

• Check your credit reports from Equifax, Experian and TransUnion by visiting annualcreditreport.com. Accounts or activity that you don’t recognize could indicate identity theft. Visit identitytheft.gov to find out what to do if there is unrecognized activity.

• Consider placing a credit freeze on your files. A credit freeze makes it hard for someone to open a new account in your name. Keep in mind that a credit freeze won’t prevent a thief from making charges to your existing accounts.

• Monitor your existing credit card and bank accounts closely for changes you don’t recognize.

• If you decide against a credit freeze, consider placing a “fraud alert” on your files. A fraud alert warns creditors that you may be an identity theft victim and that they should verify that anyone seeking credit in your name really is you.

• File your taxes early. File as soon as you have the tax information you need, before a scammer can. Tax identity theft happens when someone uses your social security number to get a tax refund or a job. Respond right away to letters from the Internal Revenue Service.

Customers can visit identitytheft.gov/databreach to learn more about protecting themselves after a data breach.

Debt Relief Specialist wants to share a settlement letter from Pen Fed Credit Union. Bal. $744.95 Offer $358.20 Savings $386.75

It’s one thing to knowingly make decisions that hurt your credit score. We’ve all been there, and sometimes tough decisions must be made. But it’s an entirely different situation to accidentally wreck your credit. After your debt program is complete pay attention to the following to help maintain a good credit score.

In some cases, we make decisions without realizing the impact on our credit. In other cases we may know that certain decisions can hurt our score, but we don’t appreciate the severity of the impact. Either way, maintaining good credit requires more than casual attention.

It is entirely possible that you could be accidentally wrecking your credit, and here are some of the ways that you could be doing just that.

1. Not Paying Attention to Your Credit Balances

Good credit is about more than just paying bills on time. About 30% of your credit score is based on your amount of debt, which includes your credit utilization. That’s the ratio of how much you owe on your credit lines divided by the total credit limit of those lines. For example, if you have total credit lines of $40,000, and you have a total outstanding balance of $10,000, your credit utilization ratio is 25% ($10,000 divided by $40,000).

If that ratio exceeds 30%, it can have a negative impact on your credit score. If you are casual about your credit balances, they can slowly creep up to 40%, 50%, 60% or more. At that point, you may see your credit scores begin to sink.

2. Closing Accounts

A lot of people make it a habit of closing out any credit cards that they pay off. From a credit perspective, however, this can have a negative impact. Though it seems counter-intuitive, a paid in full line of credit or credit card is a positive contributor to your credit score, even if you stopped using the account.

This brings us back to credit utilization. If you pay off a credit card that has a line of $5,000, that available credit is contributing to the total amount of credit you have available. That will improve your credit utilization ratio. Closing the card will lower your available credit, increase your overall credit utilization, and potentially lower your credit score.

3. Co-Signing Loans

Co-signing loans is another area where people are often very casual. They often assume that they are just doing a good deed to help a friend or family member, and may even mistakenly believe that it’s simply a one-time event.

But when you co-sign a loan, you will be involved in that loan and that loan will be on your credit report until it is fully paid. In the event that the primary borrower makes a late payment, this will have an impact on your credit score. Worse, should the loan go into default, this will also show up on your credit.

4. Applying for Too Many Lines of Credit

If you have good credit, it’s likely that you are getting bombarded with credit offers in the mail on a weekly basis. If you are in the habit of applying for the better ones every month or so, you could be unknowingly hurting your credit.

Credit inquiries account for 10% of your overall credit score. While this is the least significant factor, these hard pulls — as they are called — can ding your credit. Consider the impact these inquiries can have the next time you consider a 0% credit card offer or bonus miles sign-up deal.

5. Not Monitoring Your Credit Scores

One of the best ways to know if you are hurting your credit is by monitoring your credit scores. Credit scores change on at least a monthly basis, but typically stay within a tight range. A significant drop in your scores, say more than 25 or 30 points, is an indication that something is wrong. You won’t know about the drop, however, unless you are paying attention to your credit scores on a regular basis.

A significant drop in your score could be an indication that your credit utilization ratio is getting too high. It can also indicate an unsuspected late payment. Errors are also possible when it comes to credit. And at the extreme, a big drop in your credit score could be an indication that you are the victim of identity theft.

You won’t know any of these unless you are monitoring your credit scores on a regular basis. Unfortunately, ignorance is not bliss when it comes to your credit. You shouldn’t obsess about it, but at the same time, you should never be too casual about it, either. Bad things can happen when you’re not paying attention.

In the more than 15 years of experience working in the debt industry, I’ve heard every story under the sun about how someone fell into debt. While there are times when people fall into debt for unavoidable reasons, I do notice a lot of people fall into debt for the same reasons. So in order to help keep you from making the same mistakes, here are the five biggest reasons I’ve seen people fall into debt.

1. Treating Credit Like Cash

Many of my clients have a tendency to treat their credit cards like an extension of their bank account. They max out their credit cards without taking into consideration the impact it’s having on their Credit Scores and how much more they’re paying over time in interest. This sort of behavior could really put you in a jam!

My solution? Stick to a debit card or keep yourself honest with only one or two low-limit credit cards. I also advise them to assign specific “jobs” to their cards, to keep them from overspending. Budgeting for “fun” purchases that you pay for with cash or a debit card could help keep you from overspending, while reserving your credit cards to handle recurring bills and online subscriptions — in amounts you can pay in full each month — is a better way to manage them. Keep in mind, carrying a balance that is more than 30% of your credit limit can have a negative impact on your credit scores.

2. Trying to Keep Up With the Joneses

True wealth is having a high net worth, not having a lot of stuff. A lot of my clients fall into debt because they believe in order to seem financially successful they need to SPEND their money on elaborate, luxurious and unnecessary things to simply keep up with neighbors. Trying to keep up with appearances and maintain a lifestyle you can’t afford is one of the quickest ways to fall into debt.

So what do I tell my clients? I explain to them that the neighbors they’re so concerned with, the ones with the fancy cars, are most likely in debt themselves! You can never know who owes money and how much, so it’s important to not judge by appearances. Spend only on things you can afford, put money away and you’ll be the one people want to keep up with.

3. Not Separating Needs From Wants

You want to have your priorities straight, especially when it comes to money. Not having a clear understanding of the things you need as opposed to the things you want could result in a lot of unnecessary spending and, in turn, debt.

Whenever my clients seem to be having difficulty understanding the difference between needs and wants, I tell them to write everything down. Making a simple list of needs, wants and even a category for both can help you identify and prioritize your spending goals. Keeping a tight list can help you attend to the things you need while also setting aside enough money to get the things you want.

4. Financial Illiteracy

Some people just don’t know how money works, how to budget or how to manage personal finances. Whether it’s because they were never properly educated or simply hated economics in school, financial illiteracy can lead anyone into debt.

That said, it’s never too late to learn! I always suggest that my clients take some time and educate themselves on basic personal finance. With the vast number of great books, blogs, podcasts and websites out there dedicated to personal finance and financial literacy, you’re sure to find a way to learn about money and, subsequently, keep yourself out of debt.

5. Hoping for the Best, But Not Preparing for the Worst

Without an emergency fund, you’re leaving yourself exposed to all sorts of financial woes. I understand that you cannot prepare for every situation, but having a safety net of funds in the bank can help you sleep better and keep you from getting into debt when the unexpected happens.

A lot of my clients find themselves falling into debt when disaster strikes because they simply didn’t save enough. I suggest they build a budget so they can see how to save to their maximum potential. Once they’ve set aside enough money, they start to understand the benefits of keeping money in the bank. I constantly have clients telling me that budgeting has given them financial peace of mind.

When it comes to staying out of debt, it really boils down to paying attention. More often than not, people find themselves up to their ears in debt because they ignore their statements, are overspending because they don’t budget, and getting caught with unmanageable expenses because they didn’t save. Take the time to sit down and review your finances. Learn how much you need to save for emergencies and long-term goals and make it a habit of continually setting money aside. The more frequently you do a checkup on your finances, and the more frequently you hold yourself accountable, the less chance you’ll have of falling into debt.

It’s almost as much of a savings cliche as checking out books at the library instead of buying them: Making coffee at home is a big money saver over going to Starbucks.

It seems like a no-brainer that making coffee at home is a lot less expensive than paying someone else to make it for you, whether that’s at Starbucks, Peet’s or your local doughnut shop. It’s an easy way to bash Starbucks — which I still visit too often while still making my morning coffee at home — by pointing out the obvious savings.

Pretty much anything you do at home is going to be a lot cheaper than going out for it. That includes meals, washing clothes and growing your own produce.

What I wanted to do, after talking up the savings of making coffee at home for years, is actually add up the costs and see if it’s really worth your time. If the savings isn’t too big, such as within a dime or so, you might as well save some time and go to Starbucks or wherever each day for your cup of coffee. Your time is worth money, but sometimes it’s worth it to pay someone else to do the service for you. That’s partly how restaurants stay in business.

Before I get into the costs of how I make coffee at home, here’s a video lesson from Matt Giovanisci of Roasty Coffee (which isn’t quite yet a live site, though you can sign up for updates) on my preferred method of using a French Press:

I should point out that I’m not getting paid by Roasty to promote it, but think it’s a great idea.

The costs

A French Press can cost $ 20 to $ 50. I’ve bought a few of the $ 20, 8-cup Recycled Coffee Press by Bodum. I say “a few” because while they’re dishwasher safe, they’re made of glass and shouldn’t go on the bottom rack. Put them up high in the dishwasher, where there’s less chance of breakage.

The next big cost is coffee. I go with whole beans at Costco because buying more expensive ground beans seems like a waste of money when you can ground the whole beans for free at Costco. I pay $ 20 for a 3-pound bag, which easily lasts my wife and I two months.

Matt at Roasty recommends also having a grinder, scale and kettle at home. Those are too expensive for me. I grind my coffee for free at the store, scoop it out with a tablespoon as my measuring instrument, and heat tap water in the microwave oven.

Do the math

Now comes the main mathematical question of how much coffee can I get out of a 3-pound bag of coffee beans?

According to Askville by Amazon, the usual formula is that one ounce of coffee is used for every 16 ounces of water. A pound of coffee will make 256 ounces.

That equates to 32 eight-ounce cups of coffee.

A Starbucks Grande size is equal to 16 ounces. So my one pound of coffee at home would equal 16 16-ounce cups of coffee. Multiply that by three pounds of coffee beans, and you’ve got 48 cups of 16-ounce coffee, or 48 Grandes at Starbucks for $ 20 worth of coffee.

Divide that $ 20 by 48, and it costs 41 cents per 16-ounce cup of coffee.

A Grande Cafe Mocha at Starbucks costs $ 4.15, according to HackTheMenu, which is an order I assume people are more likely to make than the $ 1.95 Grande size of regular coffee at Starbucks.

Savings of making coffee at home: $ 3.74

The savings of making coffee at home equates to $ 3.74 per 16-ounce cup.

Here’s the math: 4.15 – 0.41 = $ 3.74.

That’s how much more it costs to buy it at Starbucks. At 41 cents per cup of coffee, my wife and I drink at home probably six days per week, adding up to $ 4.92 per week, or $ 19.68 per month.

These expenses don’t include the upfront costs of a coffee press, electricity and any extras you add to your home-brewed coffee, such as flavorings or creamer. And they surely don’t include the cost of your time.

Other benefits of making coffee at home

If the money saved by making coffee at home adds up to enough of a savings for you, then it’s worth it. But if your time is worth more than the $ 3.74 saved, then it’s worthwhile to go to Starbucks or elsewhere for your coffee.

But even with that extra time and effort of making coffee at home, I think it’s worth it to make it at home. Without getting all Zen about it, there’s something relaxing about cooking — whether it’s a complicated dinner, a simple sandwich for lunch, or a pot of coffee. There’s also the knowledge that you know exactly what’s going into your cup of coffee, and the pride in making it yourself.

This isn’t to say that an occasional trip to Starbucks or a meal out isn’t a worthy expense. We all deserve a treat.

But remember that it is an expense. Making coffee at home an average of six days per week saves me $ 3.74 per day, or $ 22.44 per week, or $ 89.76 per month, or $ 1,077.12 per year. For my wife and I, that equates to $ 2,154.24 per year in savings by making coffee at home.

That’s a lot of cash. What would you do with that cash? Spend it or save it? We throw out some options in this post.

copyright 2026 Consumer Debt Help Association - 516 N. Dixie Highway, Lantana, FL 33462. All Rights Reserved