Debt Relief Specialist wants to share a settlement letter from Lowes.

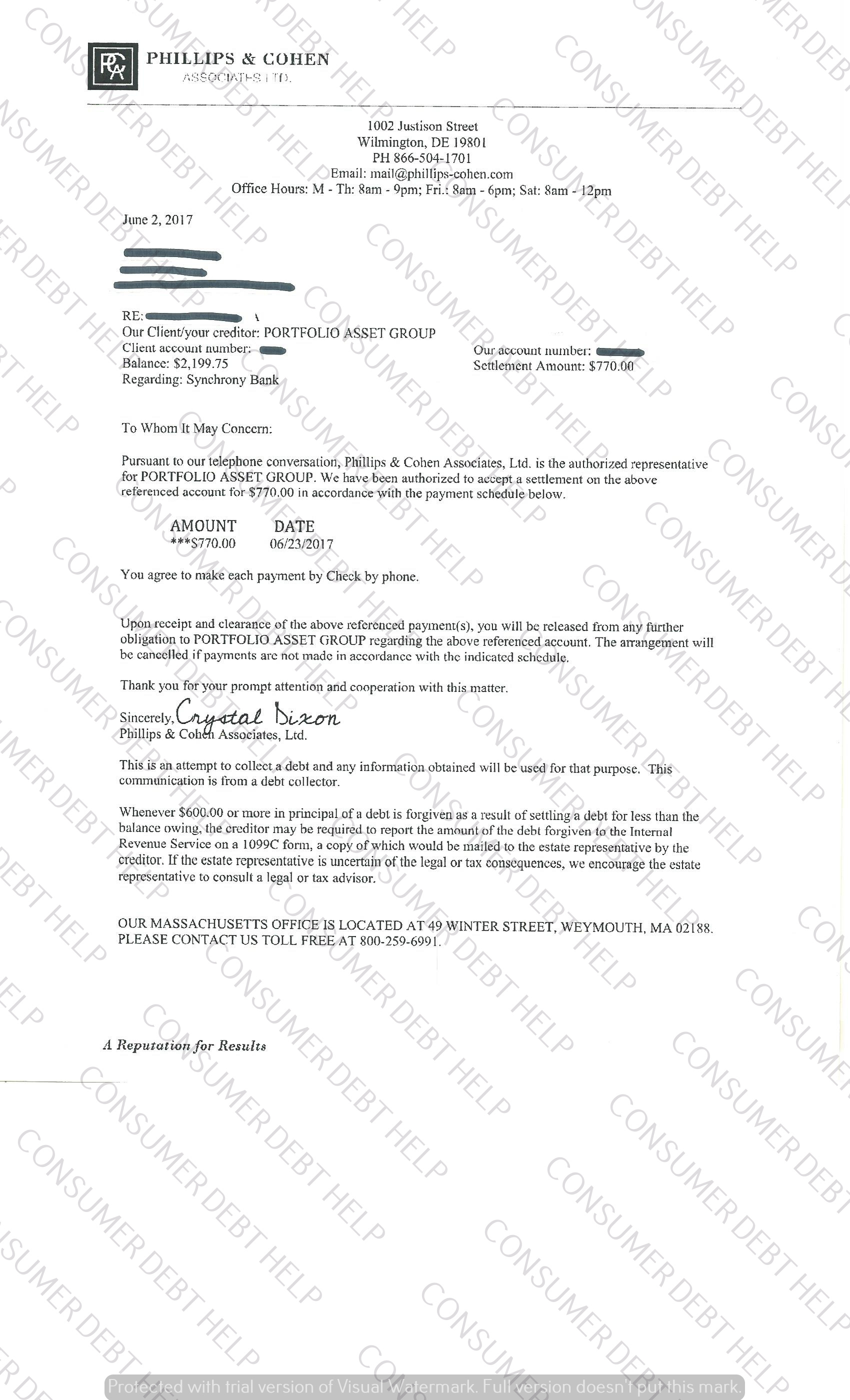

Balance:$5746.20

Offer: $1500.00

Savings $4246.20

Savings 73.9%

Debt Relief Specialist wants to share a settlement letter from Lowes.

Balance:$5746.20

Offer: $1500.00

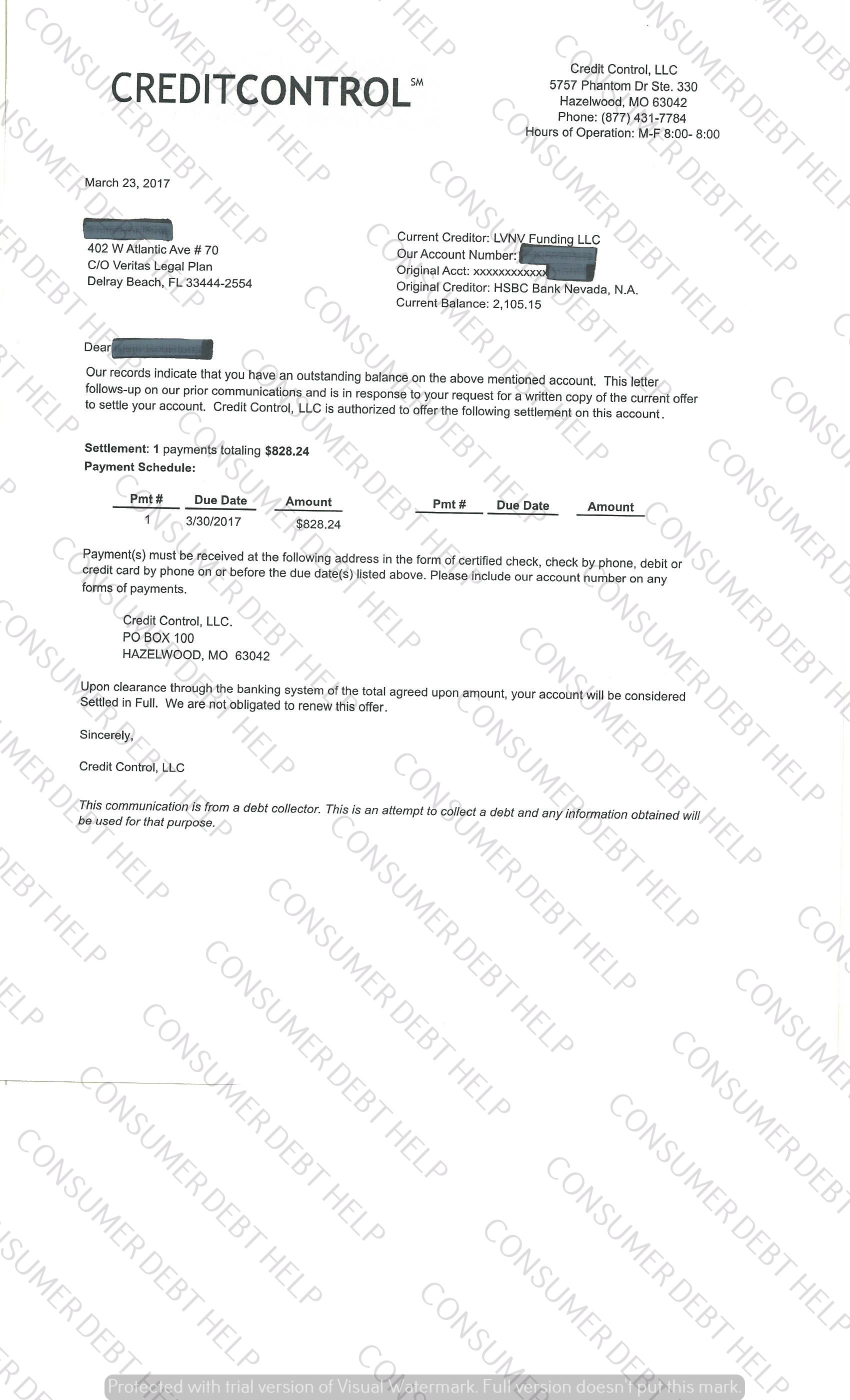

Republished here with attribution under FairUse for education and commentary

There were some 14.5 billion U.S. general purpose credit card transactions in the first six months of 2015, accounting for more than $1.4 trillion in purchase volume.27 General purpose credit card spending has risen as a proportion of gross domestic product, rising from 10 percent of GDP in 2000 to 15 percent in 2014.2

The total number of credit card transactions in the U.S. was 26.2 billion in 2012, up from 21 billion in 2009,3 according to the 2013 Federal Reserve Payments Study. Other findings from that report:

The four major credit card networks in the United States are Visa, MasterCard, American Express and Discover.

Visa is the largest. In 2014, Visa’s U.S. credit purchase volume was $1.2 trillion,5 up from $1.1 trillion in 2013.6 There were 304 million Visa credit cards in circulation in the United States and 545 million Visa credit cards in circulation outside of the United States in September 2014.5 In comparison, there were 285 million Visa credit cards in circulation in the United States and 526 million cards in the rest of the world the year before.6

MasterCard’s U.S. credit purchase volume was $607 billion for 2014,7 up from $560 billion in 2013.8 There were 191 million MasterCard credit cards in the United States and 576 million cards in the rest of the world in December 2014.7 In comparison, there were 178 million MasterCard credit cards in the U.S. and 563 million cards in the rest of the world the year before.8

American Express also saw growth from year to year, as U.S. cardholders spent $668 billion in 2014, up from $637 billion the year before. At the end of 2014, there were 54.9 million American Express credit cards in circulation in the U.S. and 57.3 million in the rest of the world. That compares to 53.1 million cards in the U.S. and 54.1 million in the rest of the world, in 2013.9

Finally, Discover had a credit purchase volume of $129 billion in 2014,10 up from $123 billion in 2013.11

In the final quarter of 2014, the 10 biggest credit card issuers in the United States had $671 billion in outstanding loans — nearly 85 percent of all the outstanding loans among more than 5,000 issuers, according to PaymentsSource.12

|

OUTSTANDING BALANCES (U.S.), BY CREDIT CARD ISSUER, Q4 2014

|

||

| Bank | Outstanding loans | Percent of overall sample |

| Citigroup | $140.746 billion | 17.8% |

| JPMorgan | $120.326 billion | 15.2% |

| Bank of America | $102.344 billion | 13% |

| Capital One | $81.024 billion | 10.3% |

| American Express | $60.737 billion | 7.7% |

| Discover | $55.941 billion | 7.1% |

| Synchrony | $39,786 billion | 5% |

| Wells Fargo | $31.119 billion | 3.9% |

| Barclays Delaware Holdings | $20.715 billion | 2.6% |

| U.S. Bancorp | $18.515 billion | 2.3% |

When it comes to the issuers with the greatest card circulation, the same companies, not surprisingly, dominate.

|

CARD CIRCULATION (U.S.), BY CREDIT CARD ISSUER, Q4 2014

|

|||||||||

| Bank | Card circulation | Percent of overall sample | |||||||

| Citigroup | 109,774,131 | 18.1% | |||||||

| JPMorgan | 93,847,656 | 15.5% | |||||||

| Bank of America | 79,822,686 | 13.1% | |||||||

| Capital One | 63,194,228 | 10.4% | |||||||

| American Express | 54,900,000 | 9% | |||||||

| Discover | 43,630,772 | 7.2% | |||||||

| Synchrony | 31,030,786 | 5.1% | |||||||

| Wells Fargo | 24,271,107 | 4% | |||||||

| Barclays Delaware Holdings | 16,156,368 | 2.7% | |||||||

| U.S. Bancorp | 14,440,681 | 2.4% | |||||||

While the Great Recession led some credit card issuers to tighten their lending standards, evidence is mixed on whether banks are embracing more consumers with less-than-stellar credit. Between January and July, the number of new card accounts for consumers with subprime credit — those with credit scores of 660 or lower — was up 40 percent over the same period in 2013, according to Equifax.14

But newer data from Experian shows the number of cards issued to subprime borrowers was roughly the same in the first quarter of 2015 as in the same period in 2014 — after rising somewhat during the middle of 2014. And the Experian data shows that credit card limits fell for people with subprime credit, from $1,171 in the first quarter of 2014 to $966 in the first quarter of 2015. (The credit limits of prime borrowers also fell during that year, from $5,382 to $5,209).20

Other findings from Equifax include:

TransUnion has also found that the number of credit card accounts is growing. In the first quarter of 2014, there were 344.53 million card accounts, up from 329.73 in the first quarter of 2013.15

However, not all segments of the credit card industry are seeing more business. The percentage of consumers using co-branded or affinity cards fell from 55 percent in 2009 to 43 percent in 2013, according to market researchers at Packaged Facts.16

One major threat that continues to impact cards in circulation is security. Card fraud losses totaled $16.31 billion in the U.S. in 2014 and accounted for 48.2 percent of global card fraud losses worldwide, according to The Nilson Report.26 Credit cards in the United States have traditionally used a magnetic stripe, but a nationwide migration to EMV payment technology is now underway. EMV is a global standard in which cards have computer chips that dynamically authenticate transactions instead of relying on easy-to-copy magnetic stripes.

Chip cards have been popular around the world for years and are currently used in more than 80 countries, according to GoChipCard.com.21 At the end of 2014, there were approximately 3.4 billion smart chip cards in circulation around the globe, per EMV Connection.22 Today, U.S. card issuers are in the midst of upgrading approximately 1.2 billion credit and debit cards to smart chip cards.25 Approximately 400 million chip cards were issued in the U.S. by the end of 2015.22

The U.S. adoption of chip cards was largely precipitated by a network-imposed EMV fraud liability shift deadline on Oct. 1, 2015. As of March 2016, approximately 70 of all cardholders had been issued at least one EMV-chipped card.23

See related: Credit card statistics, Credit card delinquency statistics, Credit card debt statistics

Scam: Caller threatens arrest if you don’t pay.

Story Highlights

In a growing scam reaching people across the country, phone fraudsters are using the threat of arrest warrants to pressure people into forking over hundreds, sometimes thousands, of dollars.

Just recently, police in Georgia, Kansas, Oregon and Florida have investigated phone scams in which a caller impersonates a local police officer. The callers, manipulating caller ID to make the number appear to come from the local sheriff’s office or jail, tell potential victims they have an outstanding warrant for an unpaid debt, missed jury duty or some minor infraction and that a fine is due.

The callers convince people to make the payments by wiring it through Western Union or buying a prepaid credit card like Green Dot and registering it online.

Police don’t notify people about arrest warrants by phone, and they don’t accept money to clear them, the Collier County, Fla., sheriff’s office said in a warning last week.

“They try to make this as convincing and as frightening as possible,” says Kati Daffan, a staff attorney with the Federal Trade Commission’s Bureau of Consumer Protection.

In Georgia’s Floyd County, Amanda Middleton, 31, paid $1,550 to clear a non-existent arrest warrant related to a payday loan she never had.

Middleton, 31, got a call saying she owed $495 for a loan. She says she checked with her creditors and found no record of the loan. She had previous debt disputes after another Amanda Middleton failed to pay off a loan, she says, so she brushed it off and told the caller to e-mail proof.

But after a second call from a so-called police officer threatening to arrest her, Middleton gave in.

“He said, ‘In our eyes, you’re just refusing to pay the debt,'” she recalls. “‘We’re just going to have to proceed forward and have you arrested.'”

Her husband checked the number; it was the sheriff’s office. Middleton paid the $495, along with a $500 fine and several “litigation fees” — a total of $1,550.

Only after Middleton sent the money through a prepaid credit card did she call the sheriff’s office and learn there was no warrant.

“I don’t consider myself to be very naïve,” she said. “We were doing what you do in that call. I called all my creditors. I asked for documentation on it. My husband called the number back. I thought we were being very careful.”

Floyd County Sheriff’s Deputy Jerry Duke says he has seen earlier versions of the scam, when so-called loan-collection agents would try to convince people they had to pay off loans. Impersonating police is a new twist, he says.

It is nearly impossible to track down scammers, Duke says. Wire transfers and prepaid cards are untraceable, and manipulated phone numbers are tough to trace.

“There’s really no recourse for them,” Duke says. “The best thing that can be done is making people aware.” Continue reading “Scam: Caller threatens arrest if you don’t pay”

copyright 2025 Consumer Debt Help Association - 516 N. Dixie Highway, Lantana, FL 33462. All Rights Reserved