Debt Relief Specialist wants to share a settlement letter from Discover Bank. Bal. $1357.59 Offer $951.00 Savings $406.59

Debt Relief Specialist wants to share a settlement letter from Discover Bank. Bal. $1357.59 Offer $951.00 Savings $406.59

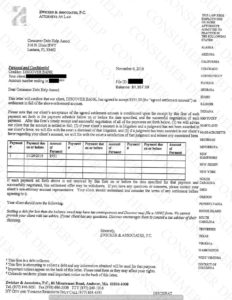

Debt Relief Specialist wants to share a settlement letter from PNC Bank. Bal. $11,724.54 Offer $3518.00 Savings $8206.54

Debt Relief Specialist wants to share a settlement letter from Capital One. Bal. $33,554.61 Offer $10,066.38 Savings $23,488.23

5 Unfair Debt Collection Practices to Watch Out For.

Luckily you are with Consumer Debt Help Association and we handle the majority of these issues for our clients, but this is what you could have expected to see or maybe you were dealing with before putting your trust in us to handle your accounts for you.

When you stop making payments on your outstanding debts, your creditor will either assign your debt to a collection agency or sell it to debt buyers who try to collect the money you owe.

They do this because your creditor has already exhausted all the means available to them to collect on the debt themselves. Since nothing worked, they sell the account at a price that allows the debt buyer to make a profit if they can successfully collect on the debt.

The Fair Debt Collection Practices Act (FDCPA) is a statute that governs third-party debt collectors. It was created to protect consumers from abusive debt collections practices.

That being said, there are a number of ways debt collectors can cross the line in their attempts to get you to pay your debt. Here are five unfair debt collection practices you should watch out for:

1. Excessive contact

Have you ever felt like debt collectors are contacting you 24/7, almost to the point where it could be considered harassment? If you are receiving an excessive number of phone calls from the same agency, this could be a violation of the FDCPA. You can present information on violations to the FTC to see if you have a case of harassment.

2. Using threats and scare tactics

Many debt collectors will resort to threats in an attempt to scare you into paying up. But here is the truth: no one can be jailed because of unpaid debt. There may be legal consequences but there must be due process first. This can be hard to ignore but do your best to stay calm and don’t let this kind of talk scare you. Instead, ask the debt collector for proof that the debt is actually yours in the form of a debt validation letter. In fact, it’s the debt collector’s responsibility to send you a written validation of your debt within five days of contacting you. Verify that the debt is actually yours rather than panicking over meaningless threats. And remember, abusive, violent threats are a clear violation of the FDCPA and you have the right to sue over these types of practices.

3. Misrepresenting their authority

Debt collectors cannot misrepresent their authority or claim to be anyone they are not. They can’t pretend to be a police officer, attorney, or even a credit reporting agency. And they are not allowed to show up at your front door and pretend to be the police. These unfair and deceptive tactics are designed to scare you into paying your debt. Stay calm and grounded in the knowledge that you have rights as a consumer.

4. Disclosing your debt to other people

Your outstanding debts are your private information and debt collectors are prohibited from disclosing that information to any unauthorized individuals. And they are not allowed to disclose in any way that they are debt collectors in their written correspondence. To do so puts unfair pressure on the consumer, especially when a third party becomes aware of the debt.

5. Violating the statute of limitations

Many consumers are unaware that there is a statute of limitations on most kinds of debt. A statute of limitations is the length of time when your creditors are allowed to take legal action on your debt. The statute of limitations varies by state and it is your responsibility to prove that the debt has surpassed the statute of limitations. It will vary based on the type of loan and in some states, the statue of limitations can be as high as 15 years.

Know Your Rights

It’s important to keep in mind that debt collectors have a job to do. They earn a commission based off of what they are able to collect from you. So it is in their best interest to take any means possible to try to get you to pay up.

But unpaid debt doesn’t give anyone the right to harass or threaten you. They aren’t allowed to expose your debt to any unauthorized third parties. And you will not be hauled off to jail because of unpaid debts.

That’s why it’s important to understand your rights as a consumer. Do your best to stay calm, remember your rights as a consumer, and take any necessary action to protect yourself, such as seeking Debt Relief.

Debt Relief Specialist wants to share a settlement letter from Citibank. Bal. $6794.37 Offer $2380.00 Savings $4414.37

Debt Relief Specialist wants to share a settlement letter from Dell Financial Services. Bal. $3045.57 Offer $1218.40 Savings $1827.17

copyright 2026 Consumer Debt Help Association - 516 N. Dixie Highway, Lantana, FL 33462. All Rights Reserved