Consumer Debt Help Association, Debt Relief Specialist wants to share a settlement letter from BJ’s/Comenity Bank. Bal. $8895.67 Offer $2670.00 Savings $6225.67

Consumer Debt Help Association, Debt Relief Specialist wants to share a settlement letter from BJ’s/Comenity Bank. Bal. $8895.67 Offer $2670.00 Savings $6225.67

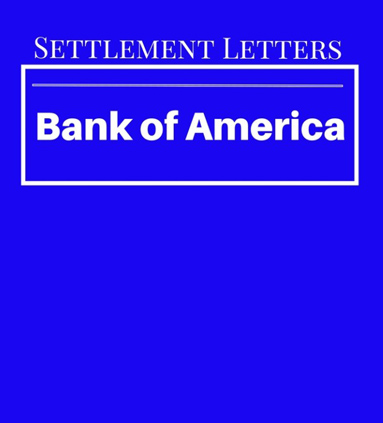

Consumer Debt Help Association, Debt Relief Specialist wants to share a settlement letter from Bank of America. Bal. $2095.95 Offer $1153.00 Savings $942.95

Consumer Debt Help Association, Debt Relief Specialist wants to share a settlement letter from Chase Bank. Bal. $2675.36 Offer $936.38 Savings $1738.98

Consumer Debt Help Association, Debt Relief Specialist wants to share a settlement letter from Lending Club/Web Bank. Bal. $7754.08 Offer $2700.00 Savings $5054.08

Consumer Debt Help Association, Debt Relief Specialist wants to share a settlement letter from PayPal/Synchrony Bank. Bal.$5732.14 Offer $1433.04 Savings $4299.10

Nearly 1 in 3 Americans expect to take on debt this holiday shopping season, a survey from Credit Karma found.

The Covid 19 Pandemic took a toll on many people’s finances, leaving them financially unprepared for the coming holiday season, according to the survey, which polled 1,020 U.S. adults in October.

On top of that, concerns about low inventory this year has shoppers starting early, and potentially missing out on deals.

With supply chain shortages and shipping delays increasing prices for all shoppers this season, it will be important for consumers to be thoughtful about their spending to ensure they don’t start the new year in the red, a chief people officer at Credit Karma, said in a statement.

Here are steps to take to help you set a budget for holiday shopping.

Talk to family and friends

You may not be the only one facing a budget crunch. Instead of buying gifts for everyone on your list, have conversations with family and friends about alternatives. That could mean perhaps picking a name out of a hat so that everyone in each group buys just one gift.

You would be surprised how many people are relieved, it takes someone bringing it up.

Make a list

Sit down and figure out who you want to buy gifts for, what you want to get and put a dollar amount around it.

Seeing it on paper can be a good exercise you really see how much you are going to spend.

After coming up with a total budget, you can make adjustments from there. It may mean spending less per person this year or cutting down your list.

Be honest with friends and family if this is a source of stress, start setting expectations that this might not be the holiday you will be able to provide.

Start saving now

While supply chain concerns have consumers worried about out-of-stock must-haves, if you wait to make purchases you can start socking away some money each week to pay for the gifts.

Let’s just say you’re making a plan over the next six weeks, are there things in your current budget that you can cut out to make room for these purchases?

On the flip side, waiting too long can result in high prices for those hard-to-find gifts. If you see a good deal now, buy it and store it away until the holidays.

Use credit cards wisely

Ideally, you don’t want to rack up debt. Yet it’s a reality for many Americans. Fully 49% of those surveyed by Credit Karma planned to pay for gifts this holiday season with credit cards.

If you need to use a credit card, do so wisely.

You can also use that credit card on apps or browser extensions that have coupons and rewards for shopping, such as Honey or Rakuten.

Only purchase what you need, especially if you are going to be paying this off over time, she added. You want to make sure you’re looking at payments you can pay down as quickly as possible.

Consumer Debt Help Association, Debt Relief Specialist wants to share a settlement letter from Chase Bank. Bal. $2766.39 Offer $691.60 Savings $2074.79

Consumer Debt Help Association, Debt Relief Specialist wants to share a settlement letter from First Premier Bank. Bal. $820.31 Offer $410.16 Savings $410.15

Consumer Debt Help Association, Debt Relief Specialist wants to share a settlement letter from Exxon Mobil / Citibank. Bal. $1033.16 Offer $362.00 Savings $671.16

Consumer Debt Help Association, Debt Relief Specialist wants to share a settlement letter from JC Penny / Synchrony Bank. Bal. $3023.95 Offer $1360.78 Savings $1663.17

copyright 2025 Consumer Debt Help Association - 516 N. Dixie Highway, Lantana, FL 33462. All Rights Reserved